The Consumer Finance Protection Bureau’s new white paper provides an in-depth look that confirms what advocates have long argued about payday and deposit-advance loans: their design means they very frequently serve as debt traps, with borrowers unable to repay, taking out repeated loans, and struggling to cover basic living expenses for months on end.

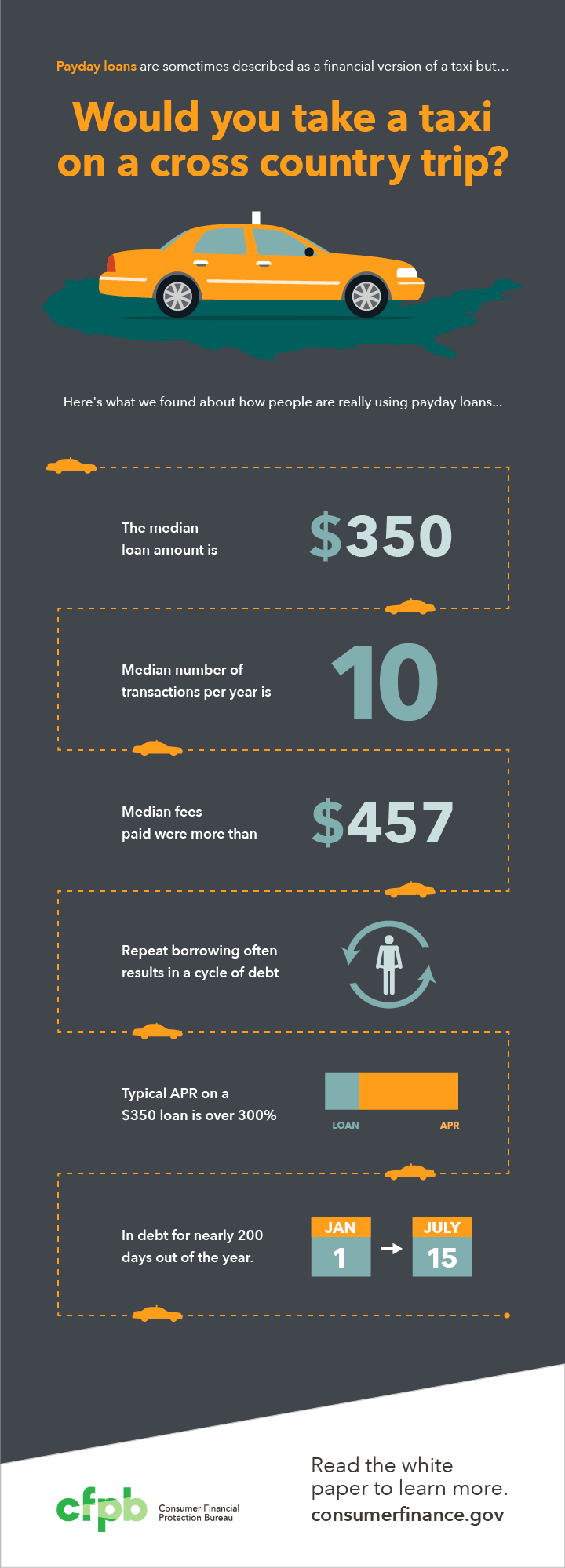

In a powerful info-graphic, the CFPB sums up the economics for a typical customer:

{kind=link}

- Amount borrowed: $350

- Transactions per year: 10

- Total fees paid: $457

- Effective annual interest: Over 300%

After a year-long inquiry the CFPB found a pattern of rollover loans leading to high fees for a “sizable segment of consumers who use these products.” For these consumers, taking out a payday loan is like using a taxi for a cross-country trip, the CFPB concluded.

Two major regulators, the FDIC and the OCC, are preparing to take action on payday lending by banks. The CFPB has parallel authority to regulate the nonbanks that still dominate this abuse-ridden market. The findings of its report argue for strong, prompt action.