Results tagged with “Hedge Funds and Private Equity”

Events

Private Equity and Private Funds

Commentaries & Press

Private Equity and Private Funds

Commentaries & Press

Private Equity and Private Funds

Commentaries & Press

October 20, 2021

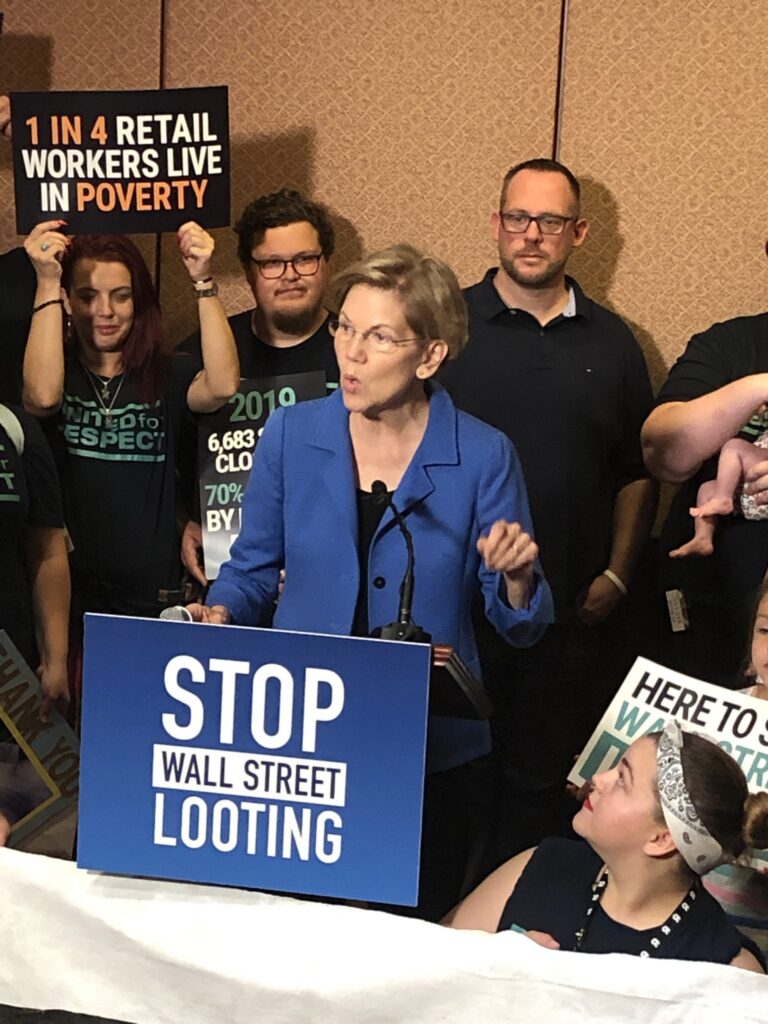

Statement: Supporters of the Stop Wall Street Looting Act

Big Banks & Wall Street Private Equity and Private Funds

Reports and Publications

October 20, 2021

Fact Sheet: Stop Wall Street Looting Act of 2021 Provisions

Private Equity and Private Funds

Reports and Publications